The WTO General Council recently decided that the next WTO Ministerial Council meeting would be held in November this year in Geneva, rather than in June in Kazakhstan as had been planned. Although normally WTO Ministerial Conferences are held every two years, MC12, as it is called, will be the first Ministerial Conference since MC11 in Buenos Aires in December 2017.

That Conference was notable for its failure, for the first time, to agree a ministerial declaration affirming the continued importance of the WTO to the global trading system. Specifically, on agriculture, there were no agreed outcomes and no agreed work programme for the future. While many countries, particularly developing countries, wanted negotiations to continue based on the Doha Round Declaration in 2001 and a single undertaking, other countries such as the US argued that this declaration was out-dated and no longer relevant.

One element of Sustainable Development Goal 2 to end hunger, achieve food security and improved nutrition and promote sustainable agriculture agreed by world leaders as part of the 2030 Agenda for Sustainable Development is a commitment to “Correct and prevent trade restrictions and distortions in world agricultural markets, including through the parallel elimination of all forms of agricultural export subsidies and all export measures with equivalent effect, in accordance with the mandate of the Doha Development Round.”

Against that background, “Members continue to emphasize the importance of an agricultural outcome at MC12 for the reform and to preserve the credibility and relevance of the Organization”, as Ambassador Gloria Abraham Peralta, Chair of the Special Session of the Committee on Agriculture where negotiations on agricultural issues take place, reported to an informal meeting of the Trade Negotiations Committee and Heads of Delegations last December (JOB/AG/191). But a successful outcome requires the political will to reach agreement, and there is no sign that this yet exists.

The purpose of post is to describe the issues that are stalling progress on the agricultural agenda, and to assess the prospects that the log-jam might be broken in the months leading up to November. This post builds on the regular detailed reports on the progress of the negotiations by the Chair of the Special Session, and particularly the assessment made by Ambassador Deep Ford when he stepped down as Chair in June 2020 and a useful assessment he made in a restricted document in February 2020. It has also benefited from recent updates on the status of the negotiations by Jonathan Hepburn of the International Institute for Sustainable Development (here), by Joseph Glauber of the International Food Policy Research Institute (here), by Anita Regmi and colleagues at the US Congressional Research Service (here), and by Peter Ungphakorn, a former WTO official on his Trade Beta blog (here). As will become clear, progress on further limiting domestic support remains the priority for all WTO Members. Here we have the benefit of a recent magisterial review of the issues by Lars Brink and David Orden published by the International Agricultural Trade Research Consortium.

Reasons for the absence of political will

There are various reasons why countries are unwilling to invest political capital in pursuing further agricultural trade liberalisation and greater disciplines on agricultural support.

First, the politics of trade liberalisation is usually played out within countries, with export industries in favour and import-competing industries against. In the post-war period, the gains to export industries have usually been sufficiently great to ensure support for trade liberalisation.

In the case of agriculture, the divisions tend to be between exporting and import-dependent countries rather than within them. For import-dependent countries without an export sector, there is no domestic constituency in favour of trade liberalisation (and the tariffs facing those developing countries that have a significant export sector in, for example, agricultural raw materials, tropical beverages, vegetable oils or fruits are often low so there are no real advantages to be gained from further liberalisation in any case). The EU and US, with large diversified agricultural sectors, have important export interests but also sensitive sectors that would be vulnerable to imports so are clearly exceptions to this generalisation. Nonetheless, agricultural exceptionalism was sufficiently strong that it kept agricultural trade liberalisation off the trade agenda for the entire post-war period until the initiation of the GATT Uruguay Round in the mid-1980s.

Second, the outcome of the Uruguay Round was an agreement, for the first time, to liberalise agricultural trade and to introduce disciplines on agricultural support and export subsidies. The extent to which liberalisation occurred was modest. The more important outcome of the Agreement on Agriculture was that it set limits on future levels of tariffs and support. It also provided an architecture or framework (the three pillars of market access, domestic support, and export competition) within which discussions on further liberalisation could take place.

This success arose in a context where international agricultural trade was dominated by two major players, the US and the EU, that were bleeding huge sums of taxpayers’ money on subsidisation of their exports in competition with each other. Once these two players saw the futility of this exercise and agreed on a cease-fire in the Blair House Accord in November 1992, the way was opened for the Agreement on Agriculture as we know it today. Reforms to date mean that competitive export subsidisation no longer brings the same pressure for a further agreement. In fact, for much of the period since the Doha Round was launched in 2001 food prices have been quite volatile with sharp peaks, as in 2008, 2011 and in recent months. This has given greater weight to consumer interests as compared to producer interests in the agricultural policy debate.

Third, rapid changes in agricultural markets and in the landscape of agricultural support have changed the dynamic of the agricultural negotiations. The growing importance of China, India, and other emerging economies has led to rapid growth in South-South trade and has called into question the relevance of the traditional division between developed and developing countries and the case for special and differential treatment (SDT) for the latter. Over half of all trade-distorting agricultural support is now provided by countries that self-elect as developing countries (Brazil and South Korea have both declared they will no longer seek developing country status in future negotiations in response to US cajoling and threats, respectively, but this does not affect their existing commitments that are based on developing country status).

Although the WTO is founded on the principle of non-discrimination, SDT is accepted as a legitimate principle recognising that not all countries start from an equal position. Developing countries face particular needs and historical disadvantages. This justification loses force when countries that designate themselves as developing prove to be highly competitive exporters and gain a significant share of world agricultural trade. On the other hand, a successful trade performance can go hand in hand with large numbers of low-income farmers farming very small plots where many live close to or under the poverty line. This can justify a continued need for policy space to allow for interventions designed to support markets and incomes for these farmers. Some WTO Members want to limit the ability to self-elect as a developing country using formal criteria, while others are unwilling to accept any change to existing practice. This question of which countries would be asked to make bigger concessions in establishing new disciplines on market access restrictions or domestic support adds a further layer of complexity to the negotiations.

A fourth reason for the lack of political will is that many developing countries see the Agreement on Agriculture as heavily favouring the ability of richer, developed countries to provide support to their farmers while unreasonably limiting the scope for developing countries to provide such support. This outcome was the result of applying a formula which used existing levels of support as the starting point to set limits on future support. Even if such a formula required larger reductions in bound limits for those countries that historically provided the highest levels of support, it still leaves them with a greater ‘entitlement’ to support than countries which historically provided very limited support and which committed to maintain these low levels.

This sense of unfairness is mainly directed to the disciplines on domestic support. Although the actual outcome is more nuanced than outlined in the previous paragraph, it is the case that the Agreement on Agriculture rules give greater scope to many developed countries to provide particular types of support than many developing countries (this is further discussed below). Thus, for many developing countries, the key objective for the next stage of the agricultural negotiations is to rebalance commitments on domestic support, implying that mostly developed countries should make concessions without seeking or getting anything in exchange. Whatever the objective merits of this argument, it is politically an impossible sell to domestic constituencies.

A fifth reason for the lack of political will to achieve a negotiated outcome at MC12 is that major players have shifted their focus from the multilateral arena to seeking to conclude bilateral or regional preferential trade agreements. These agreements can deliver some limited market-opening for agricultural trade, although of their nature they are unable to address disciplines on agricultural support (for example, the recent EU-UK Trade and Cooperation Agreement explicitly excludes agricultural subsidies from the scope of its disciplines on state supports generally).

A sixth reason that makes progress on the agricultural agenda difficult before MC12 are the reverberations of the COVID-19 pandemic. On the one hand, this has highlighted the potential damage that restrictions on exports of food can cause for importing countries, and it has re-energised calls for greater transparency and disciplines on the use of export restrictions. The pandemic has also seen a sharp rise in farm aid packages particularly in developed countries. The potential impact of these farm supports on world markets has caused alarm but has also strengthened arguments regarding the need for greater policy space to respond to emergency situations of this kind. On balance, the uncertainty generated by COVID-19 and the responses it has engendered have probably made countries less willing to tie their hands with respect to agricultural support than they might have been before.

Issues in the negotiations

Agricultural negotiations in the WTO take place in the Special Session of the Committee on Agriculture. Following the failure of MC11 to agree a work programme, the Chair of the Special Session, Ambassador Deep Ford of Guyana, proposed a new working process around seven priority issues: domestic support, public stockholding (PSH) for food security purposes, cotton, market access, the special safeguard mechanism (SSM), export competition and export restrictions. While all these issues are important, making progress on domestic support is seen as the key issue by all countries.

Domestic support

Calculating trade-distorting domestic support

Trade-distorting support is measured by an Aggregate Measurement of Support (AMS). This is defined as the level of support provided for an agricultural product in favour of producers of the product (product-specific support) as well as support provided in favour of producers in general (non-product-specific support), other than support that is exempt from reduction because it meets the criteria of Annex 2 of the Agreement (Green Box). Adding up the AMSs for individual products and for non-product-specific support yields the Total AMS.

However, in making this calculation the Agreement allows some other categories of support to be ignored and excluded from the Total AMS. In addition to the Green Box, the other excluded categories are de minimis amounts (5% of the value of production for product-specific support plus 5% of the total value of agricultural production for non-product-specific support, 10% and 10% respectively for developing countries and 8.5% and 8.5% respectively for China and Kazakhstan), Blue Box payments and, for developing countries only, generally available investment subsidies as well as agricultural input subsidies generally available to low-income or resource-poor producers. WTO Member commit to keep their Total AMS calculated in this way below their scheduled entitlement under the Agreement.

The rules on domestic support are perceived as unfair because, while most countries have a zero AMS entitlement, a few countries have a positive AMS entitlement because they provided high levels of trade-distorting support in the past. There are 32 countries with positive AMS ceilings. While over half of these are developing countries the EU, Japan, US, Canada, Switzerland and Norway between them make up 87% of the total value. A zero AMS entitlement means that the amount of trade-distorting support a WTO Member can provide to its farmers is limited to those categories which are not counted towards its Total AMS. Countries that have a positive AMS entitlement have an additional degree of leeway. Another advantage is that this positive AMS can be focused on one or a few products, thus permitting effective product-specific support well in excess of the 10% (or 5%) limit for countries with a zero AMS entitlement.

Trade-distorting support is primarily support linked to either production, inputs or prices. Market price support is provided when a government purchases product at a guaranteed minimum support price. Another bone of contention is that the formula used to calculate market price support can have anomalous outcomes that do not make economic sense. The formula used multiplies the quantity of product eligible for support by a price gap. The price gap, in turn, is the difference between the value of the administered support price and a fixed external reference price based on the world price in the base period for the Agreement 1986-1988.

Because of the sharp rise in nominal prices since the Agreement on Agriculture entered into force, this formula can show the existence of apparent market price support if the administered support price is greater than the external reference price (which must be counted towards the product’s AMS) even where the administered support price is below the current world price (where, in an economic sense, no support is provided to producers). Several countries classed as developing, including China, India and Turkey, have exceeded their domestic support commitments in recent years.

Trends in domestic support

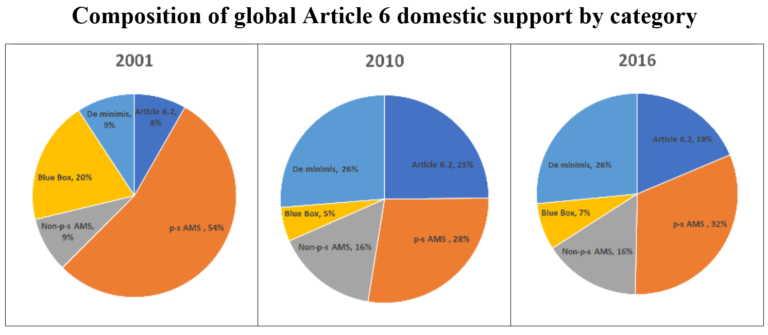

Trends in the use of trade-distorting support are shown in the following two diagrams. Trade-distorting support is defined as all support covered by Article 6 of the Agreement on Agriculture except for support exempted by virtue of Annex 2 (Green Box) because it has no or minimal trade-distorting effect. Thus it includes AMS support (Amber Box), de minimis support, Blue Box, and support exempted from reduction commitments by virtue of Article 6.2 (Development Box). Data for three years are shown: 2001 which is the first year of China’s membership, 2010, and 2016 which is the latest year for which domestic support notifications for all major Members are available. The latest developments in farm payments as a result of the Covid-19 pandemic are obviously not covered by the data in these figures.

Figure 1 shows the changing composition of trade-distorting support (TDS) over time. To set the figures in context, global TDS has changed relatively little over the period. It was $106 billion in 2001, $116 billion in 2010 and $122 billion in 2016. De minimis, Article 6.2 support and non-product-specific AMS support has grown over time, at the expense of Blue Box support and product-specific AMS. As it is mainly developed countries that have access to AMS support, and it is also developed countries that mainly use the Blue Box, Figure 1 is a first indication that TDS has been rising more rapidly in developing countries (which are mostly limited to using de minimis and Article 6.2 support) relative to TDS in developed countries. Most of this change occurred between 2001 and 2010, with relatively little change in the relative importance of the various support categories in the more recent period.

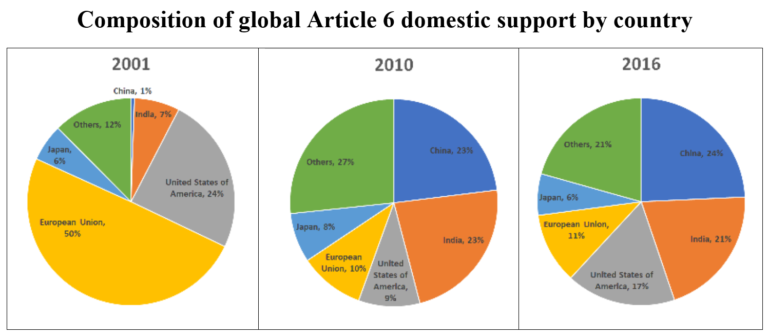

This is confirmed if we examine the composition of global TDS by major WTO Members shown in Figure 2. Around 80% of TDS is due to the five major Members separately identified in the figure. Strikingly, in 2001, the EU accounted for half of all global TDS, one indicator of the malign impact that the CAP had on world markets at that time. However, CAP reform under Agriculture Commissioners Fischler and Fischer-Boel, through the decoupling of previously coupled payments, has significantly shrunk the EU contribution. The other main feature of the figure is the rapid increase in the share of global TDS now provided by China and India, while the US share, having shrunk considerably in the first period, has grown again in the second period.

China and India provide large amounts of TDS in absolute terms partly because they are large countries with large agricultural sectors. If instead TDS is expressed as a proportion of a country’s value of agricultural output, the rankings look very different with small countries with a strong comparative disadvantage in agricultural production at the top of the league: Iceland with a share in 2016 of 72%, Norway with 52%, Switzerland with 13%, Japan with 12%, and Israel and Canada with 8% each. The figures for the US are 8% and for the EU 5%. For China and India, on the other hand, the figures are 3% and 10%, respectively, in 2016 (again, these proportions combine Article 6 and de minimis support in the Canadian tool to calculate TDS).

Disciplining domestic support

Even if there were a common objective to reduce TDS, Members have put forward a wide range of proposals as to how this might be done. Some focus on reducing existing limits (on AMS support, on Blue Box support, on de minimis) while others focus on introducing a new limit on Overall Trade Distorting Support (OTDS). For example, a joint proposal from Brazil, EU, Colombia, Peru and Uruguay in July 2017 proposed to set an OTDS limit covering AMS and de minimis support (with the treatment of Blue Box support left to be decided) as a fixed percentage of the value of agricultural production in a base year, with developing countries allowed to have a higher percentage (plus continued access to Article 6.2 support). Australia and New Zealand in October 2017 put forward a proposal to limit OTDS support (defined as all Article 6 support including de minimis payments and Article 6.2 support) to something close to what countries actually used in a base period. A counter-proposal from China and India in June 2018 proposed the elimination of AMS support entitlements for developed countries starting with a phasing out of product-specific AMS support. These proposals differ both in their ambition but also in terms of the countries that would be asked to make the largest concessions.

Although not a priority in the current discussions, there have also been calls to review, revise and strengthen Green Box disciplines. Some of the impetus for this comes from a concern over ‘box-shifting’, where countries have not necessarily reduced farm support but have instead reformed it so that it qualifies as a Green Box measure. Arguably, this was precisely the intention of the Agreement on Agriculture, not to prevent countries from providing farm support if this was a domestic policy objective, but to ensure that this support did not distort trade to the detriment of other trading partners. However, the sheer size of Green Box support in some countries linked to the view that these payments do have some production effect has prompted calls for stronger disciplines on some categories of Green Box support. There has also been a concern whether the existing Green Box disciplines are sufficiently flexible to accommodate support to farmers to encourage more environmentally-friendly and climate-friendly farming practices in the future.

Public stockholding for food security purposes

The way in which the measurement of market price support for the purpose of calculating a product’s AMS may lead to counter-intuitive results seen from an economic perspective was previously mentioned. To be clear, the Agreement on Agriculture specifies that expenditure on building food security stocks at market prices and, for developing countries, disposing of food at subsidised prices to low-income households, is a Green Box measure and is not limited in any way. However, it also specifies that, where stocks of foodstuffs for food security purposes are acquired and released at administered prices, the difference between the acquisition price and the external reference price should be accounted for in the AMS.

India, which operates a significant food reserve programme of this kind, has long argued that the purchase of food stocks at minimum prices for food security purposes should be exempt from AMS disciplines. It has been supported in this position by the G33 group of developing countries. For India and other proponents, the fear is that, if they must account for the gap between these administered prices and their fixed external reference prices, they would likely exceed the product-specific limit of the 10% de minimis of total production in some key products. This is made virtually certain by the general uplift in food prices since the 1986-88 base period used to set the fixed external reference price. For non-proponents, the risk is that stocks built up based on minimum prices might subsequently be exported at less than the acquisition price, leading to the disruption of commercial markets.

At MC9 in Bali in 2013, WTO Members agreed to an interim ‘peace clause’ that exempted any support provided through existing PSH programmes for traditional food staples from challenge, provided that the country met certain transparency provisions and committed to ensuring that stocks procured under the PSH programme do not adversely affect trade or the food security of other Members. The conference also agreed to work towards a permanent solution that would be open to all developing countries by MC11, and that the interim solution would remain in place until a permanent solution was found. As noted, no solution was agreed at MC11 so the interim arrangement remains in place. India invoked the Bali Decision for the first time in its domestic support notification for the marketing year 2018-2019 submitted in March 2020.

Cotton

Cotton has had a special status in the negotiations since the WTO General Council recognised in 2004 that cotton “will be addressed ambitiously, expeditiously, and specifically, within the agriculture negotiations.” This responded to a cotton initiative reflecting the importance of cotton in the export earnings of a handful of least-developed countries in West Africa that are the main proponents of this initiative. Under the 2015 Nairobi Ministerial Decision on Cotton, exports of cotton and cotton-related products from least developed countries should have duty-free and quota-free access in developed country markets and in developing countries in a position to provide this. Cotton-specific trade-distorting support, notably provided by the US and China, is thus the central element of the negotiations on cotton. Although disciplines on cotton-specific support could be addressed separately to domestic support in general, it seems there has been very limited engagement on this issue in the agricultural negotiations to date.

Market access

Reductions in high tariffs, particularly on ‘sensitive’ products such as beef, dairy and rice, remain an objective of agricultural exporting countries. However, there is no expectation of any immediate progress on further tariff liberalisation. The majority of WTO Members have defensive positions in this pillar. Instead, the focus has been on enhancing transparency and facilitating agricultural trade without altering the core tariff commitments in Members’ schedules. The elements under discussion include applied tariffs transparency and treatment of shipments en route, tariff simplification, and transparency of TRQ administration. Other issues that have been raised include tariff escalation, tariff peaks, access for tropical products, and the status of the Special Safeguard. The existence of considerable binding overhang (i.e., a large difference between countries’ bound tariffs and the tariffs they actually apply) suggests some scope to lock-in tariff reforms that countries have already undertaken, but such overhang is not distributed evenly across all WTO Members. Discussions have not begun on a possible tariff reduction modality.

Special Safeguard Mechanism

WTO Members have agreed that developing countries should have access to a Special Safeguard Mechanism (SSM) to counter the negative impacts of import surges and price surges. Disagreement over the technical parameters (trigger, remedies, duration, etc.) was one of the principal reasons why negotiations on the Revised Modalities proposed by then Chair of the agricultural negotiations Crawford Falconer broke down in 2008. A Ministerial Council Decision at MC10 in Nairobi authorised the continuation of negotiations on this topic but there has been no real progress since then.

Disagreement over the purpose of the SSM is one major block to progress. Developing country proponents see it as linked to their broader food security objectives, designed to protect their poor and vulnerable farmers from import surges and sudden price declines. For non-proponents, the SSM is linked to progress on market access reforms. This group rejects any notion that the SSM could result in tariffs being raised above the levels bound in previous negotiations. In recent discussions, proponents have argued that the challenges the SSM seeks to address arise largely because of trade distortions and heavy agricultural subsidisation. Non-proponents have indicated their willingness to enter technical discussions on the design of an SSM that would not penalise exports of countries that do not engage in agricultural subsidisation. The fact that a small group of WTO Members (mainly developed countries) have access to a Special Safeguard (SSG) resulting from the tariffication process at the end of the Uruguay Round that provides similar protection to what developing countries seek in the SSM is taken as another example of how the existing Agreement on Agriculture rules are unbalanced with respect to developing countries.

Export competition

The Nairobi Ministerial Council Decision on Export Competition which mandated the elimination of export subsidies has been one of the few WTO negotiating successes since the end of the Uruguay Round. Some countries still see unfinished business under this pillar, including disciplines on export finance, on international food aid, and the need to minimise the trade distorting effects of the export monopoly power of state trading enterprises. However, these issues are not subject to active negotiations at the moment.

Export restrictions

Several countries imposed import restrictions on food exports because of the Covid-19 pandemic (although it should be noted that liberalising measures on food trade outnumber restrictive measures). This has raised the relevance of this issue in the negotiations. Singapore introduced a proposal that would exempt from export restrictions food purchases for humanitarian purposes by the World Food Programme. It was hoped this might be adopted by the WTO General Council at its meeting in December 2020. This did not happen due to objections by India and several other countries that were concerned that such purchases could adversely affect the food security of the supplying country, even though the proposal was explicitly amended to take this objection into account. Subsequently, 53 WTO Members signed a unilateral declaration committing not to impose export prohibitions or restrictions on foodstuffs purchased for non-commercial humanitarian purposes by the WFP. The failure to agree on this ‘trust-building’ measure is just one indication of the difficulties in making progress on the agricultural agenda.

Future prospects

The postponement of MC12 to the end of this year gives a little more time to address some of the differences that are stalling progress on the WTO agricultural agenda. Are there indications that this could lead to progress on some of the issues outlined above?

The installation of a new Administration in the US with a greater declared willingness to seek multilateral solutions to global issues is a positive sign. However, this in itself does not indicate that the new Administration will take a different view regarding US interests. Despite the apparent contempt of the Trump Administration for the WTO, the US continued to play an active role in addressing the agricultural agenda with a string of proposals on specific issues under discussion. The Biden Administration may be willing to invest more effort in seeking solutions, but its substantive demands may not be very different.

The EU can be a positive force for progress. In its recent Trade Policy Review, it asserted that “support for effective rules-based multilateralism is a key geopolitical EU interest”. It shares US concerns that WTO disciplines are inadequate to address the role of the state in China’s economy, and on the need for greater targeting of special and differential treatment. Successive CAP reforms have reduced the EU’s use of trade-distorting support. Although it continues to have very high tariffs on sensitive products, there is now a large overhang between its scheduled AMS ceiling and its actual AMS use. This allowed it to propose in 2017, along with Brazil and some other Latin American countries, a new discipline on Overall Trade Distorting Support (OTDS). In the Annex to its Trade Policy Review on WTO reform, the EU highlighted again that it is in favour of a substantial reduction in trade-distorting domestic support.

The role that China will play remains ambiguous. China made very considerable concessions, not least in its agricultural commitments, at its accession to the WTO in 2001. It still elects to see itself as a developing country at the WTO, thus benefiting from special and differential treatment. However, taking a wider view, President Xi Jinping has on various occasions, most recently during his intervention at the World Economic Forum at Davos in January this year, stressed his support for multilateralism. China’s success in avoiding a recession due to Covid-19 in 2020 and its rapid rebound this year suggests that it will become the world’s largest economy by 2028, five years ahead of the previous estimate. Already we see how this new status has influenced China’s climate policy when President Xi Jinping committed his country to achieving climate neutrality by 2060 at the UN General Assembly meeting in 2020. If China saw an opportunity where its influence might be decisive in moving along agricultural negotiations at the WTO, this could indeed be a game-changer.

Finally, there is India, the awkward member of the Big Four. India has played a spoiling role at recent WTO meetings which has won it few friends. But India has good reason to believe that current WTO rules unfairly work against its interests. As noted, India submitted a domestic support notification for the marketing year 2018-2019 in which it noted that its product-specific support for rice exceeded its de minimis level. This was the result of its minimum support price when purchasing for its public food reserve stocks being well above the fixed external reference price used to calculate the rice product AMS.

Yet the OECD Producer Support Estimate database, which measures economic support to different products, reports that the transfer to rice producers in India was -9.83% in 2018 and -17.38% in 2019. In other words, India’s minimum support price was well below world market prices in those years and there was no economic support to rice producers. Indeed, there has been a negative transfer to rice producers in India in nearly all years since 2000 when the OECD started its measurements. In fact, India’s total PSE for all crops has been negative in every year that the OECD has measured since 2001. It is no wonder India feels aggrieved when other countries challenge it for providing unreasonable amounts of trade-distorting support to its producers.

Given this context, there should be scope to come to an agreement on public stockholding that would meet the concerns of both proponents and non-proponents. An agreement on PSH would help to lance the poison created by this issue and might open the door to a wider-ranging agreement on domestic support. This would require concessions by both the US and China. I don’t hold my breath that this will happen, but it suggests there could be a way forward if not in the coming months at least in the years ahead.

This post was written by Alan Matthews

Photo credit: Tom Page, via Washington International Trade Association, CC licence.

O artigo foi publicado originalmente em CAP Reform.

Discussão sobre este post