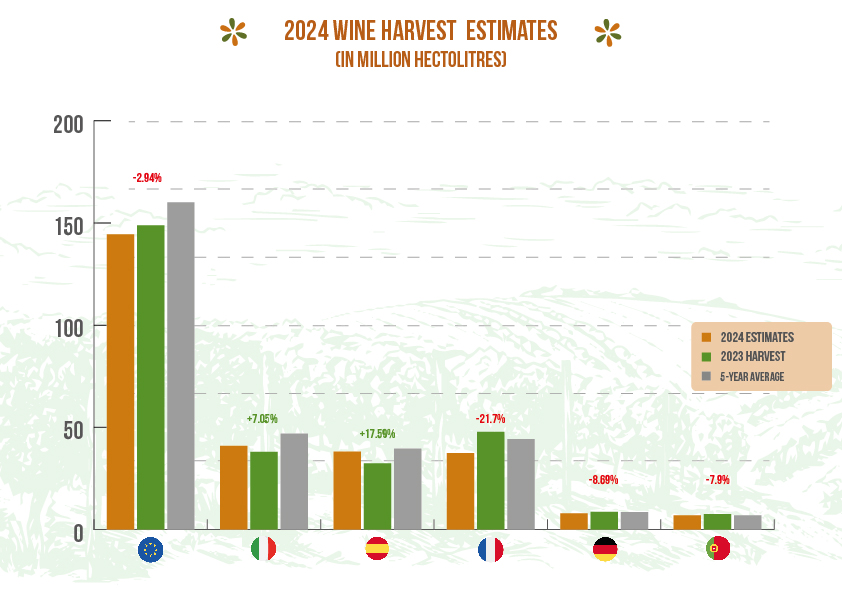

The European wine sector is reporting an estimated 144 million hectolitres (Mhl) of wine and must production for 2024. This represents a slight decrease of almost 3% from the previous year and 10% below the five-year average. This decline reflects the ongoing challenges the sector faces, particularly in terms of adverse climatic conditions.

- Italy: Leading with an estimated 41 Mhl, surpassing last year’s top producer.

- Spain: Securing second place with a considerable 18% increase in production, totalling 38.1 Mhl.

- France: Falling to third place with a significant 22% drop in production, totalling 37.4 Mhl.

Among the major EU wine-producing countries, France, Germany, and Portugal experienced declines in production compared to 2023, with decreases of 21.7%, 8.7%, and 7.9% respectively. Conversely, Italy and Spain saw increases of 7% and 17.6%. Despite these increases, all major producers fell short of their five-year average production, continuing a downward trend since the 2019 harvest.[1]

The 2024 season was marked by unpredictable weather and the lingering effects of recent droughts, leading to inconsistent harvests across regions. While constant monitoring and fieldwork helped manage plant health, widespread plant diseases were less of an issue compared to 2023. Water scarcity impacted southern regions in particular, causing early harvests in many areas.

Additionally, inflation and rising supply chain costs (including glass, gas, transport, and fertilizers) have significantly increased production expenses. The rising cost of borrowing has also made it challenging for producers to access credit for the essential investments needed to develop their businesses.

Crisis measures implemented in some member states have helped alleviate market pressure, with monitoring ongoing to assess their impact. As domestic demand continues to decline, the importance of exports to third countries has grown, making promotional measures crucial for market stability.

Luca Rigotti, president of the Copa-Cogeca’s working party on wine, commented, “This year’s production figures only confirm the market trend. The European wine market is navigating a difficult and complex period, with high production costs and international dynamics affecting the market. However, I remain optimistic about the resilience and entrepreneurship of our farmers.”

The 2024 wine season highlighted the significant challenges faced by the European wine producers, including climatic uncertainties and economic pressures. Despite these obstacles, the resilience of producers and strategic discussions in place provide cautious optimism for the future of European wine sector.

*Austria, Belgium, Bulgaria, Croatia, Cyprus, Czech Republic, Denmark, France, Germany, Greece, Hungary, Ireland, Italy, Lithuania, Luxemburg, Malta, Netherlands, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden

Source: Aggregated data from internal survey, OIV, Eurostat, national ministries, European Commission

FRANCE: A relatively low harvest for France, which after finishing first place on the podium of last year as the world’s biggest producer, now comes in third. This data follows two main trends: On one hand the ever more difficult climatic situation that sees French vineyards struggling with the management of water (too much or too little depending on the area), and the impact of droughts in previous years which have weakened vineyards. For most of the vineyards, the flowering took place in chill and humid conditions, leading to “coulure” (flower and berry drop) and “millerandage” (the formation of small grapes). Moreover, episodes of frost, mildew, and hailstorms have contributed to the reduced harvest. The grubbing up policy that the profession and the government have been putting into place has not yet had a real impact on production, with the exception of the Bordeaux region. The new program of definitive grubbing that will concern up to 30,000 ha, will have an impact on the 2025 harvest. “The 2024 campaign was challenging for French vineyards, with some areas experiencing drought and others excess water and disease, leading to significant variations in yields, and some producers losing their entire crop. The government’s support for the grubbing-up plan helps to adjust production potential, addressing demands from professionals. However, there is also a need for temporary grubbing-up measures, which have been requested for several months.”, commented Ludovic Roux, President of the Vignerons Coopérateurs d’Occitanie and Vice-president of the Copa-Cogeca working party on wine.

ITALY: Italy looks likely to re-gain the first place of world’s biggest producer, with 41.5 Mhl (estimated) of wine and must. This represents an increase compared to the previous year’s harvest, while still 12% lower than the five-years average. It has been a difficult harvest with a clear split between the north and the south of the country: In the north, the bad weather conditions (episodes of hailstorms and intense rain during spring), have increased the work in vineyards, necessary to assure their health and escalated worries about the development of plant diseases.

Contrary, the south has suffered a strong drought which affected the performance of the vines and increased worries about the future. The sporadic heavy rainfall in August has not compensated for structural water scarcity and led to the bringing forward of harvest operations. Overall, nationally the expected quality of the harvest is very high compared to the previous year, where extended episodes of downy mildew affected a good part of the vineyards. By region, the north is expected to produce an increase of 0.6% compared to the previous year, the central regions +29.1%, while the south and islands a +15.6%.

SPAIN: Regardless of the difficult weather conditions (drought), Spain is, together with Italy, the only major producer EU country to show positive signs this harvest. Climate change is moving the start of the harvest to earlier in the year, with some areas having started the harvest in the second half of July. The increase in production is mainly due to the good performance of the vineyards of the Castilla-La-Mancha region, which represents more than half of national wine production and increased its wine production by 23% compared to last year, while other regions like Cataluña, Comunidad Valenciana, Aragon, and Murcia region will follow last year’s trend or slightly lower due to sever water scarcity.

GERMANY: The reduced production in Germany compared to last year (-8.7%) has been caused by the challenging weather conditions. German vineyards experienced some stress in the first half of the year: frost in some regions, and exceptionally rainy weather all over Germany led to reduced yield (especially in the Saxonia and Saale-Unstrut regions, where the production drop reached up to 80 % of the potential). The humid conditions increased the risk of mildew and oidium infections, and a consequent increase in the labour effort in the vineyards. Contrary to forecasts, good grape material was harvested, and an excellent vintage is foreseen. Due to the good water supply, vines store a lot of minerals, which lead to the production of wines rich in extract and minerality. The long ripening phase also had a positive effect on the development of aromas in the berries. “We believe that white wine from Germany in particular has the potential to meet the current tastes of consumers this year,” stated DWV Secretary General and Vice-president of the Copa-Cogeca working party on wine, Christian Schwörer.

For the countries which represent a smaller fraction of European wine production for the 2024 harvest, Portugal, Austria, Romania, The Netherlands are expected to experience a serious reduction of their wine production, with a decrease of, respectively, 8% (to 6.9 Mhl), 19% (to 1.87 Mhl), 25% (to 3,7Mhl), and 45% (to 7 000 hl) relative to the previous harvest. This reduction in production was caused by the freezes in spring and the hot and dry summer, the wind frosts in April, the failed blooms and the heavy rains in June, as well as some odium and Peronospora episodes.

Fonte: Copa Cogeca