With harvesting already begun in the south of Europe and the weather conditions requiring a hasty harvest in the majority of Member States, Copa and Cogeca have today in Brussels presented their consolidated forecast for the cereal and oilseed harvest. According to the initial forecasts from the agricultural organisations, 2020 is expected to be a mixed year, with notably wheat and rapeseed suffering a significant drop in production.

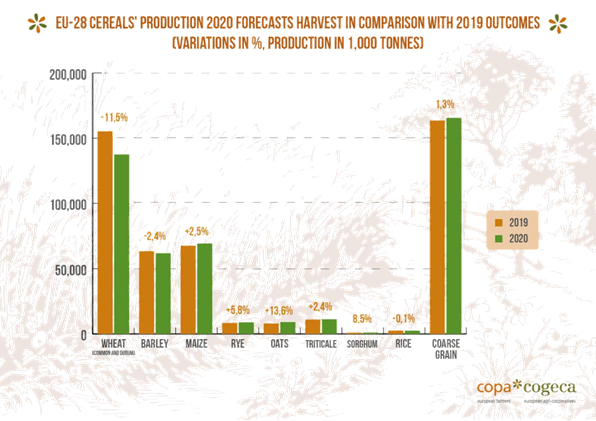

For cereals, total EU-28 production should reach the average of the previous five years with around 305 million tonnes. However, for wheat, a net decrease in total production of 11.5% is expected as a result of the twofold effect of the decrease in surface area (-3.5%) and the low level of yields for both soft and durum wheat

(-8.3%). Autumn sowing was strongly affected by the large amount of rainfall, autumn sowing varieties such as winter wheat were substituted with spring varieties such as spring barley, oats

and maize. The expected drop in incomes is mainly due to the unfavourable planting conditions, the lack of water recorded since spring and infestations of insects that are vectors of viruses. It comes as no surprise that this is reflected by an increase in production costs, mainly due to plant protection products most notably used to combat diseases and insect infestation.

Jean-François Isambert, the president of the working party on cereals, commented on the results, saying that “even if there are uncertainties surrounding these initial forecasts, we are extremely concerned about the impact of the decrease in wheat production combined with the forecast recession of the global economy on the incomes of cereal producers for the marketing year 2020/2021.”

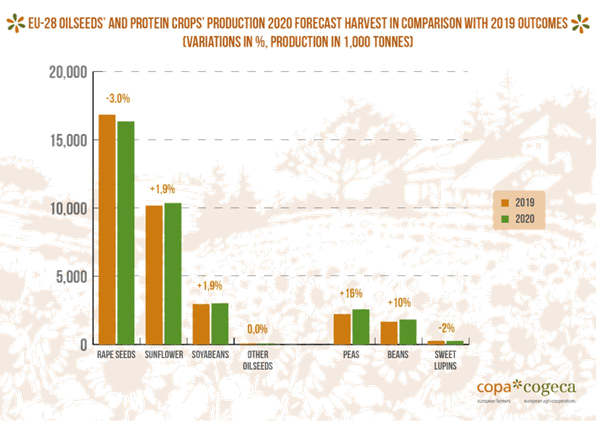

For oilseeds, total EU-28 production is expected to continue to decrease and fall below 30 million tonnes. The is mainly due to the 4.5% decrease in rapeseed surface area following the drought in certain countries as well as the excessive rainfall at the time of autumn sowing combined with high pressure from diseases and pests in a situation where the means to combat them are more and more restrained. Yields are expected to be similar to 2019, limiting EU-28 rapeseed production to 16.3 million tonnes.

Pedro Gallardo, president of the working party on oilseeds, said that he believed this historically low level of production was the result of the European policy approach to rapeseed in the past years: “We have capped biofuels, but we are ignoring the impact of limiting our consumption on co-production of protein, while we tolerate “imported deforestation” from third countries. Rapeseed producers have, amongst other things, had to combat diseases and pests, which proved to be particularly resistant this year. Due to the European and national authorities’ inability to obtain a renewal of the authorisations for a number of plant protection products as well as the absence of efficient alternatives such as new genomic techniques, it is increasingly difficult for European farmers to produce rapeseed.” If it persists, this reduction in surface area could increase our need to import protein-rich raw materials for animal feed, which would go entirely against the ambitions the Commission announced with regard to developing European protein production. A significant decrease in surface area could also threaten the viability of beekeeping in some European regions.

A slight increase of soya and sunflower surface area by 1.4% and 1.5% respectively has most notably compensated the decrease in rapeseed, due to their advantage of being spring crops. Sunflower seed and soya production are expected to increase by 1.9%.

The protein crop sector has seen an increase in sowings of 6%, rising from 1.582 million hectares to 1.674 million hectares. It is too early to comment on the expected yields. According to Pedro Gallardo, “this increase in surface area can be explained by winter crops not being grown and an increasing demand for plant protein, notably in the organic sector and due to new dietary habits.”

Discussão sobre este post